Perimeter Solutions Report

I recently did a longer-form writeup on Perimeter for an internship position I applied to. Thought I would share it with everyone (4/11 update: made slight revisions/modifications, particularly around founder fees and my DCF). Feedback is welcomed! 3 point summary below:

Perimeter’s fire safety business has a strong moat and an excellent business model

Climate change is leading to an increase in wildfires and thus demand for both reactive and proactive fire suppresion products

The ludicrously high fees owed to the founders over the next several years as well as a potential market newcomer reduce the company’s viability as an investment.

Ticker: $PRM

Price (As of 4/12): $11.10

Market Cap (As of 4/12): $1.8B

Original Twitter Thread (more concise)

Business History/Overview:

Perimeter Solutions has existed since the early 1960s under various names as a subsidiary of a range of chemical and manufacturing companies. In 2018, it was bought out from Israel Chemicals by SK Capital. In 2020, Everarc Holdings was formed by Nick Howley (longtime Transdigm CEO) and Will Thorndyke (Author of The Outsiders and partner at PE firm Housatonic Partners). Everarc was similar to a SPAC but had a unique structure in which no shareholder votes or redemptions took place in the SPAC and de-SPAC processes. Everarc took Perimeter Solutions public on the NYSE in Q4 2021.

Perimeter has two main segments. The first is Oil Additives. Perimeter manufactures the chemical P2S5, otherwise known as phosphorus pentasulfide. This chemical is mostly used in certain engine lubricants but also has use in pesticide and mining chemicals. Oil Additives are responsible for 25% of YTD revenue.

Perimeter’s second segment is Fire Safety. The company manufactures fire retardants and foams that help combat various types of fires, including wildfires, structural fires, flammable liquids fires, and more. Perimeter also sells specialized equipment and services (such as delivery, storage, and repair) alongside these products to further meet customer needs. Fire Safety is responsible for 75% of YTD revenue. This write-up will focus mostly on the fire safety side of the business as it is the company’s strongest and fastest growing segment.

Business Quality:

OA: Perimeter’s Oil Additives Segment is essentially an OEM in a fragmented market. They are one of many companies that produce P2S5 and have no competitive advantages to speak of. Management suggests that it is a lower margin business than fire safety but does not give exact figures. My calculations using y/y changes in sales and COGS suggest that gross margin for oil additives is around 14%.

Fire Safety: Perimeter’s fire safety segment is much more exciting. As previously mentioned, Perimeter sells a variety of fire-fighting retardants, foams and associated services. Retardant and retardant services make up the majority of Perimeter’s sales, accounting for 86% of fire safety revenues and 62% of overall sales in 2020. Perimeter’s main customers are the US Forest Service and other state and local governments. Many, (if not all) of these customers only use Forest Service approved products. Below is the current list of approved products:

Every product on the list (except the two underlined in red, which will be covered later) is a Perimeter Solutions product. No other company has a product fully approved for use by the Forest Service. Because of this, Perimeter has almost a total monopoly on retardant foams for wildfire suppression in the US. Countries outside of the USA often use the Forest Service’s list as an alternative to spending money to create their own testing process, so Perimeter’s domestic dominance aids them internationally as well.

It’s hard for would-be competitors to enter the market for a number of reasons. The process of getting a product approved by the Forest Service is long (3-5 years) and somewhat capital intensive (usually mid six figures). If a company were to make it past that stage, Perimeter still has an advantage due to its supply relationships with customers. The tanks and other services that customers use to store, mix and transport retardants in are often owned by Perimeter, meaning that would-be competitors have to spend even more initially in order to create their own storage and transportation equipment for use on tarmacs and air bases across the country. The company also has a history of defending its moat through fold-in acquisitions, as well the usage of intellectual property rights (with 66 total patents across the world).

To sum up Perimeter’s monopoly, here is a quote from CEO Eddie Goldberg: “No one other than $PRM has sold a commercially significant amount of retardant and not one historical would-be competitor is active today”.

In addition to having a strong product moat, the fire safety business is similar in quality to VMS (vertical market software) businesses like Constellation Software or Aspen Technology. There is less than 1% customer churn for retardants and Perimeter’s overall annual capex is 2-3% of revenues. Fire retardants are a vital part of the fire suppression process, yet make up only a low single digit percentage of customer fire safety budgets. This gives Perimeter fantastic pricing power. Another CEO quote sums this up nicely: “Once you gain a retardant customer, you almost never lose them and you almost always grow them”. Perimeter expects to grow their EBITDA margin by 1-2% a year due to pricing power and their customer/supplier relationships. Margins are already high, with overall gross and operating margins at 50 and 23 percent respectively.

Growth Prospects:

OA: The oil additives that P2S5 is used in are primarily intended for cars made in the 1980s-early 2000s. In 2021 this segment will exhibit HSD y/y growth due to mean reversion from the pandemic, but the oil additives market is expected to stay relatively flat over the coming years and as a result little-to-no revenue growth is expected.

Fire Safety: Management lays out three primary sources of revenue growth: continued growth in wildfire prevention spending, increased “wildland-urban interface”, and increased firefighting aircraft capacity.

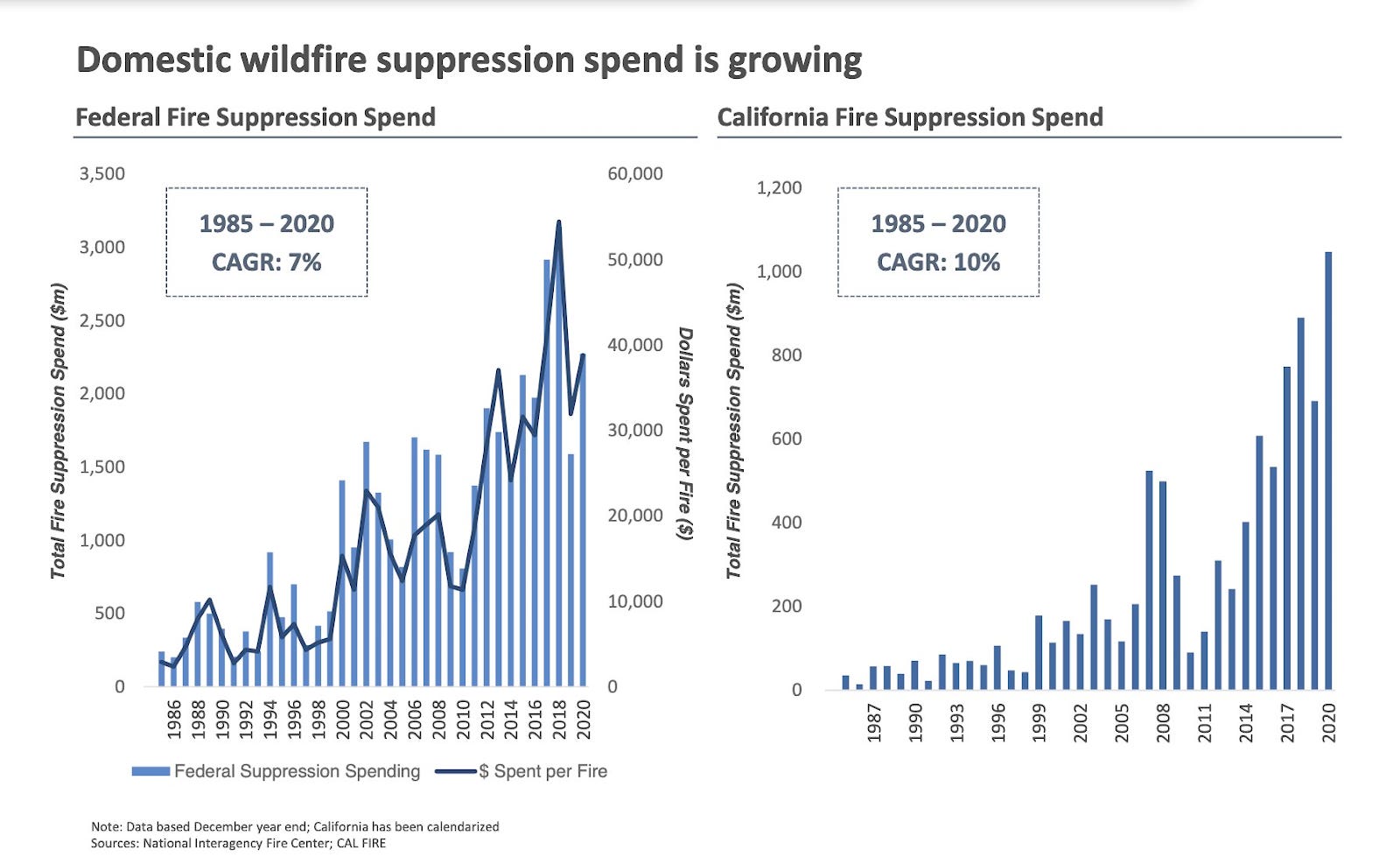

Wildfires have become increasingly prevalent in recent years due to climate change and other factors. California fire spending alone has ~6x'ed since 2010. Studies have predicted a range of results, but the growth in acreage burned in coming years is generally expected to continue or increase. That trend is also true internationally, with countries like Australia and Spain increasing similarly high growth in wildfires, which will lead to greater demand for retardant. Increasing wildfire suppression spend is probably the factor that will be most responsible for Perimeter’s growth.

Wildland-urban interface is essentially the amount of wildland that is near civilization. This has been increasing steadily over the past several years due to increased vacation home purchases and the general expansion of the American populace into new areas. This leads to increased retardant usage because firefighters now need to save areas that were completely wild and untouched by humans before but are now near newly-constructed homes and other buildings.

The third factor in revenue growth is increased firefighting aircraft capacity. Simply put, as new technology allows planes to carry more weight, they will carry more retardant in order to effectively fight fires. Thus, firefighting agencies will buy more retardant.

The only other factor I see affecting revenues is $PRM’s recent LaderaTech acquisition. They bought the company for $25mm in early 2020. The company had developed initial plans for a product now sold by Perimeter as Phos-Chek Fortify. While almost all of Perimeter’s other products are involved in fire suppression, Fortify is intended to be a proactive suppressant and prevent fires from initially combusting. This may be particularly useful along roadways or utility lines where companies seeking to avoid massive fire damage will be willing to pay for protection in advance of wildfire season. On a recent Tegus call, the co-founder of LaderaTech said he could see 2,500 miles of roadside being treated in the future (assuming inter-agency cooperation between firefighting and highway departments, which is definitely not a given). This product is the first of its kind, so adoption will be slow and Fortify will probably not make a sizable impact on revenues for the next several years.

Management:

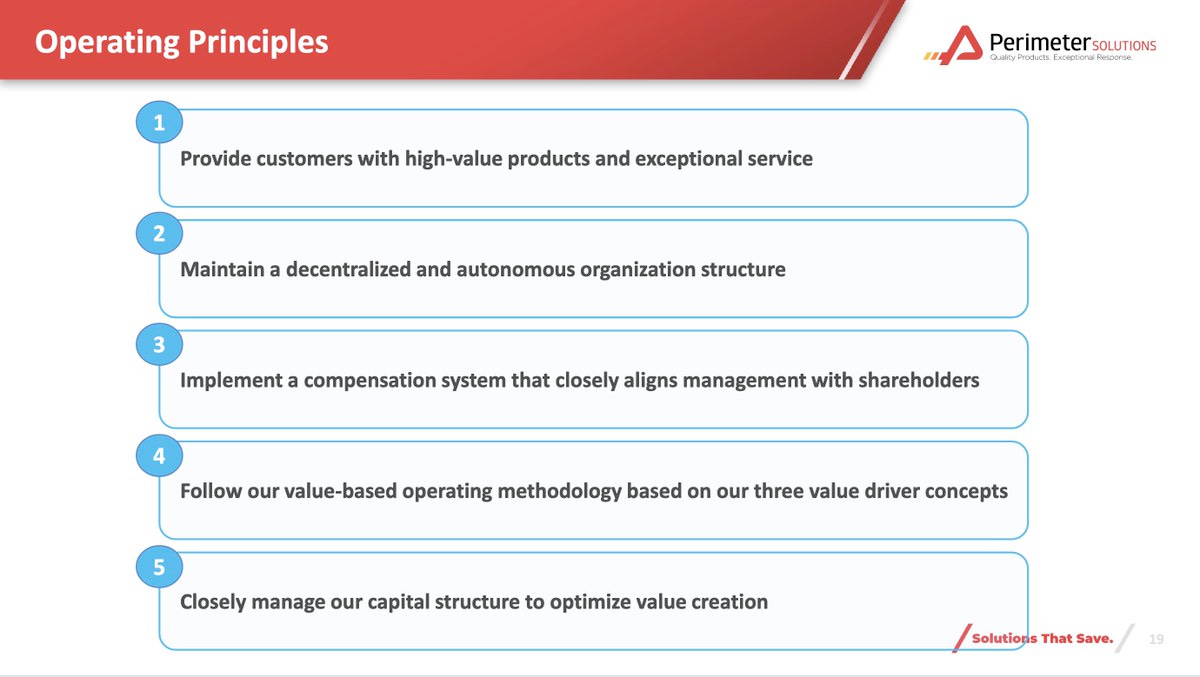

Perimeter’s CEO is Eddie Goldberg, who has been CEO since the company’s PE purchase in 2018. Goldberg has over 18 years of industry experience, and has a history of successful fold-in acquisitions (LaderaTech being a good example). Of course, one of the most interesting aspects of this company is the presence of Howley and Thorndike on the BoD. Their effect can already be seen - the below slide from a recent presentation appears to be almost directly taken from The Outsiders.

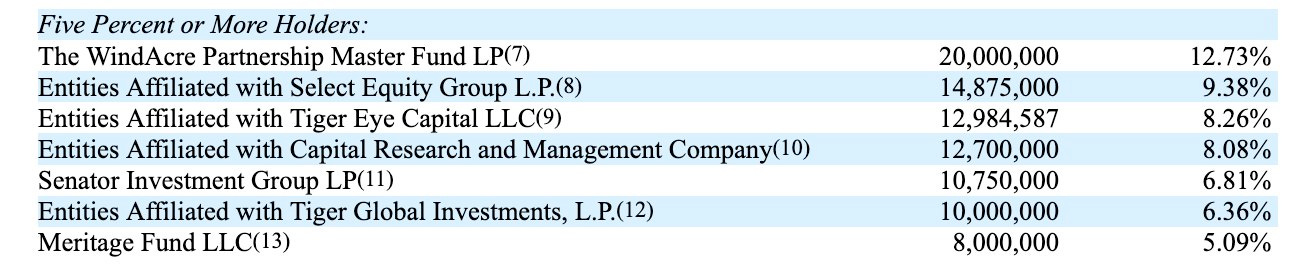

Unfortunately, Howley and Thorndike each initially own only $7-8 million in stock, which is disappointing given their knowledge of equity-based incentives. Other large holders (presumably through the PIPE, which has a one year lockup) are shown below. In their earnings presentation the company mentioned potential for further fire safety m&a, other unrelated m&a, buybacks, and special dividends as ideal uses of capital to generate FCF.

Update: It was pointed out to me that on page 4 of the Founder Advisory Agreement another incentive structure is laid out for Howley and other founding members of the SPAC. It appears to be similar to a 1.5/18 hedge fund fee structure, although with the caveat that the founders can choose to receive their compensation in combinations ranging between 100/0 and 50/50 shares/cash percentages.

Risks & Valuation:

Risks:

Perimeter’s fire safety revenue is highly volatile due to the unpredictable nature of wildfires. Although wildfires have broadly increased over time, outlier years can still be had. 2019 was a good example of that. There was an unusually low amount of acres burned that season, and as a result Perimeter had $100 million less in revenue than a comparable year like 2020, leading to an overall loss of $42 million. This could present a danger in the future as Perimeter is somewhat highly leveraged and several unusually bad years in a row could be brutal for the business. This quarter-to-quarter revenue cyclicality might be somewhat mitigated by international expansion because fire seasons are different in other countries (Australia in particular).

Another risk Perimeter has is losing market share. As mentioned previously, a competitor is 1-2 years away from being added to the Forest Service’s qualified product list. Fortress is a fire safety startup that uses magnesium chloride instead of ammonium phosphate (what Perimeter uses) as the main ingredient in their retardants and advertises it as being much more eco-friendly. Fortress recently announced a $45m investment from mineral company Compass Minerals International ($CMP) that values the company at $100 million, (~5% of $PRM's market cap). Perimeter’s largest acquisition has been for $25 million, so it may be hard for it to simply buy out Fortress. Two of Fortress’s products are in the final stage of testing before release in 2022 or 2023 while their others are slightly further behind. I have been unable to discern if Fortress’s product is any better or cheaper than Perimeter’s or if it’ll have any success in overcoming the barriers to entry I previously described.

Finally, climate-friendly legislation that forces Perimeter to change or discontinue products is always a potential (though small) risk. The Forest Service incorporates environmental damage in their testing, but critics have been complaining for years about the effect retardants have on local plant and wildlife. Here is an article on said concerns for further reading. However, PRM has experienced a similar situation before. Over the last decade or so, many state & local governments legislated out firefighting foams containing chlorine. Perimeter was ahead of the curve in upping their standards and didn’t lose any market share so I imagine they are already on top of any potential future legislation.

While not necessarily a day-to-day business success risk, the founders’ compensation plan is a massive liability to any investment thesis. Perimeter paid $652 million dollars to the founders last year in advisory/incentive fees (roughly 1/3 of current market cap), leading to a net loss of $667 million for the company. The fee structure of 1.5/18 has no carry, which means that for every $1 that the share price goes up year over year, PRM owes the founders $28 million dollars - equivalent to ~25% of Perimeter’s 2021 operating expenses (not including the $652 million in SPAC grift fees). This will last through 2027. Furthermore, the founders will receive a total 2.36 million shares a year (1.5% of original shares outstanding) through 2031.

Valuation:

I made a DCF model for the company using an 8% WACC, 3% terminal growth rate, 0% growth in oil additive revenue, 9% fire safety revenue growth, a 1% EBITDA margin expansion (guided at 1-2% by management), and other assumptions management guided towards below. 9% revenue growth is not conservative - that assumes Fortify doesn’t gain any substantial market share. If wildfires increase in size even more than expected we could see 10 or 11% revenue growth but 9% is already pretty high. 1% fire safety EBITDA margin expansion is similarly optimistic; this assumes that the company will be able to pass the higher input costs that it currently faces through to the state and local governments it deals with - not an easy task. Perimeter recently announced a $100 million buyback program, presumably to buy back the shares it has to issue to founders, but I found that modeling the founder fees through share dilution to be easiest, and used an average 4% dilution a year as an estimate for both the fixed advisory fee and any performance related fees over time.

The result was a target price of $12.73 a share, representing a 15% upside. Anyone reading this should also factor in the strong possibility that I may have no idea what I’m doing. 15% does not offer enough of a margin of error for me to invest personally, and I am neutral on the stock at current levels. I initiated a small starter position after discovering the company in late 2021 but sold after the egregious founder fees were pointed out to me. I would consider building a position in the $8-9 range, especially considering the core fire business downside risk is somewhat uncorrelated to economic conditions. I’ve included a screenshot of my Excel model below (sidenote: hopefully the formatting is up to par - this is my first attempt at an at least somewhat-professionally formatted DCF). Please feel free to reach out if you’d like to see the Excel sheet itself or have any feedback on my thesis.

Thank you for reading, and feedback is always welcomed, either in the comments here or via Twitter @EBITimDuncAn.